Bastian Teichgreeber | Chief Investment Officer | Prescient Investment Management | mail me |

A few weeks into 2022, an underlying investment theme started to emerge, that of a continued, broad-based recovery with strong economic performance across the globe.

Evidence of this recovery was noted in the U.S. Federal Open Market Committee (FOMC) January 2022 statement. Participants confirmed that due to vaccination progress and strong policy support, indicators of economic activity and employment in the U.S. had continued to strengthen.

While the sectors most adversely affected by the pandemic had improved, they continued to be affected by waves and variants of the virus. Most importantly, job gains in recent months were solid, and the unemployment rate had declined substantially.

A comprehensive global recovery and strengthened economic performance bodes well for riskier assets in the year ahead and gives us a good reason for optimism. But what factors do we see as strongly positive?

The results of in-depth internal monitoring and analysis of economic themes, inflation dynamics, labour market trends and market behaviour reveal three primary factors driving the global recovery; namely, the abating impact of COVID-19, followed by very healthy consumer balance sheets in the developed world, as well as full order books and depleted inventories within global industrial sectors.

COVID-19’s waning impact

Looking ahead, we hold the belief that the worst of the pandemic is behind us, with most economies having reopened or in the process of reopening.

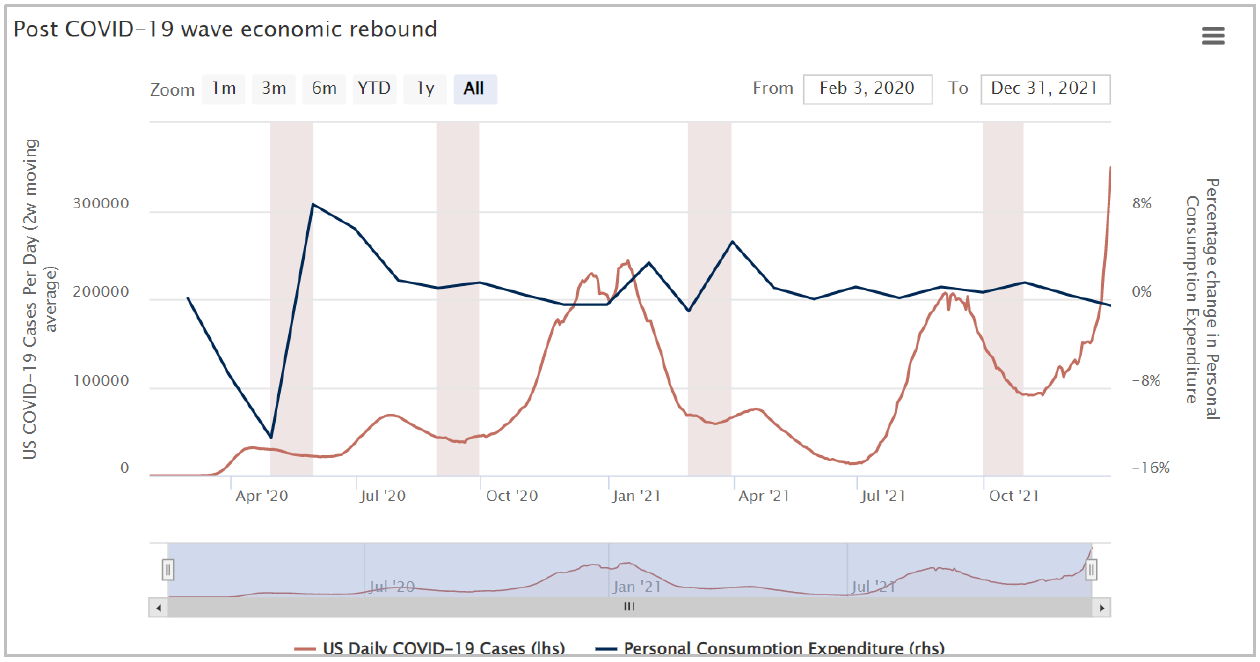

When COVID-19 first struck in March 2020, consumption in the U.S. fell sharply. Yet, the pandemic has exerted less of a drag on economic performance with each subsequent wave than before. Although the winter COVID-19 waves of 2020/21 put greater strain on global medical systems, consumption merely contracted in the following waves.

As well as the limited loss in consumption, we’ve learnt that economic activity can bounce back quickly once restrictions are eased, as consumers regain the confidence to venture out as before, assuming medical risks have been contained.

As illustrated in the chart, when looking at the change in U.S. consumption compared to daily U.S. infection rates over the last two years, it is clear that with each consecutive wave, the impact of the virus on consumption diminished and that economic growth quickly rebounded to previous levels.

Source: Prescient Investment Management, Bloomberg (as at 31 December 2021)

Healthy consumer balance sheets

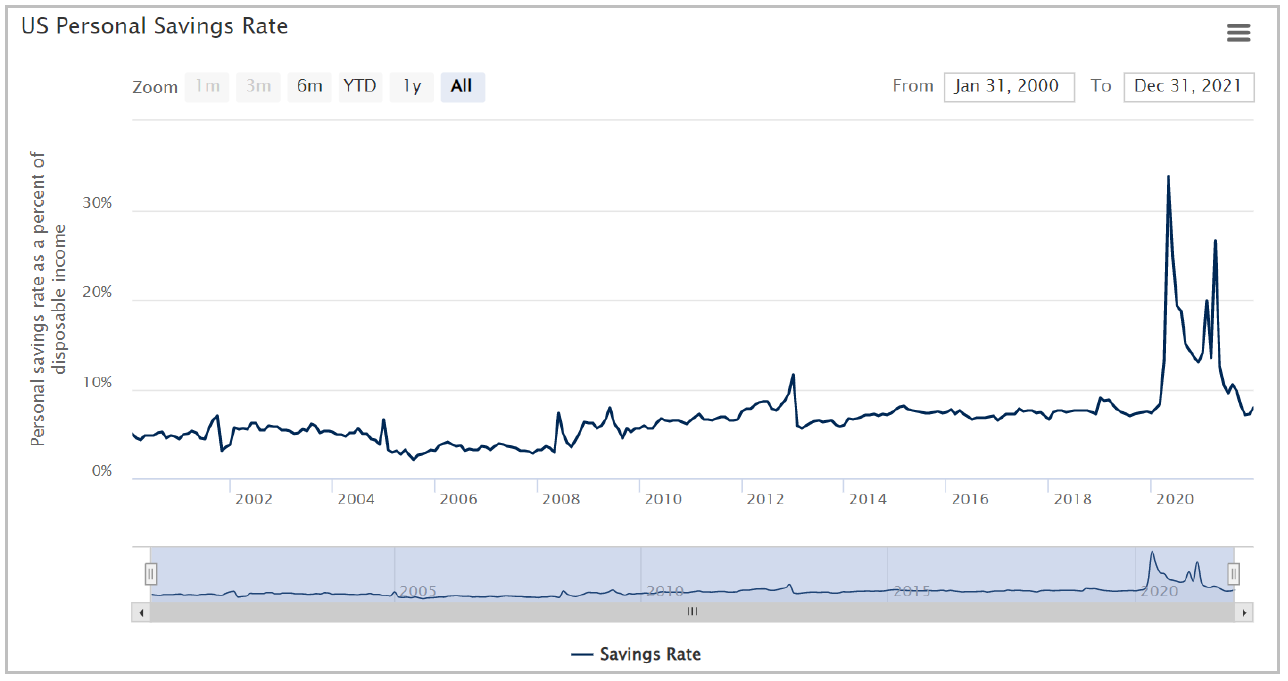

The record surge in household savings rates across the globe gives us another great reason for optimism.

At the start of the pandemic, household spending declined considerably due to restrictions on movement and social distancing measures, as well as the temporary closure of many brick-and-mortar businesses.

However, the government support that followed – in the form of generous government transfers such as stimulus cheques and other benefits – led to a rise in excess savings in the developed world of 19% of pre-pandemic annual private consumption in the U.S.

The chart below shows the savings rate as a percentage of personal income in the U.S. and illustrates an unprecedented spike that has not been reversed.

Source: Bloomberg (as at 31 December 2021)

We also do not even expect households to spend most of their excess savings wildly. However, healthy balance sheets give them a comfortable cushion against the drag of higher energy costs, less depressed mortgage rates or possible fluctuations in equity prices.

Households appear eager to spend more. Helped by the significantly positive wealth effects over the last two years, which were driven by strong asset class returns, particularly in global equity markets, they can afford it. Very strong and healthy labour market demand adds to and emphasises this theme, boosting spending power further.

Full order books and depleted inventories in industrial sector

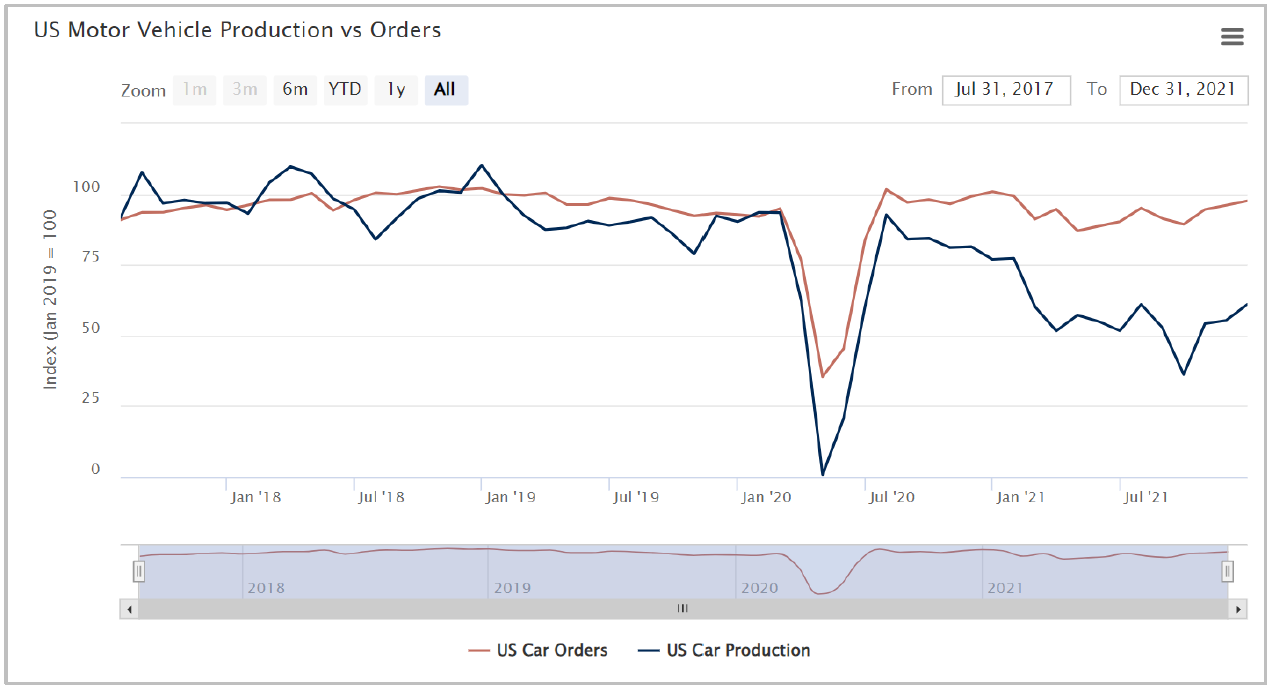

Last but not least, an in-depth analysis of corporate investments reveals further hope in the form of full order books in the industrial sector. As consumer spending looks set to rise substantially further, businesses must invest in increasing their capacities to replenish inventories.

The chart below compares U.S. Motor Vehicle Production to U.S. Motor Vehicle Orders. It shows how, up until mid-2020, the two lines tracked each other closely, as carmakers dovetailed production with new orders.

Post the COVID-19 crash, however, a clear gap between the two lines became apparent as orders started to come in at a much higher level than was being produced. This highlights the caution deployed by corporations in delivering on new orders by running down inventories.

With supply chain issues likely to be easing in 2022, it will allow for the completion of outstanding orders and offer businesses an opportunity to invest in increasing order book capacity and replenishing diminished inventory levels.

Source: Bloomberg (as at 31 December 2021)

Although we remain positive about the global economy, it’s evident that the situation we are facing in 2022 is very different to that of last year. Firstly, the slope of the yield curve has flattened significantly since its peak in March 2021. Secondly, the flattening occurred for a somewhat disturbing reason; a higher discount rate at the front end, which points to a Federal Reserve lift-off and potentially tighter financial conditions in the year ahead.

In conclusion

There is more to markets and asset class returns than economics. We advise investors to rely on a set of factors, including valuation metrics, a close assessment of financial conditions, but also careful and point-in-time gauging of investor and market sentiment. This allows for adaptability to remain well-positioned for any challenges the future holds.

Moving forward, while we are becoming more cautious on emerging and developed market equities, we believe investors would be wise to turn to risk assets, including South African equities, South African bonds, and the rand – a call that has paid off for us.

revolution?")

{kind=link}